The Distribution Arc: How Long Does It Take a Hit Film to Go Free?

Reelgood analyzed 1.93 million availability windows across 240 platforms (US market) to quantify the streaming industry’s best-kept open secret: the windowing clock is accelerating, and the data tells a different story than most licensing teams assume.

Key Takeaways

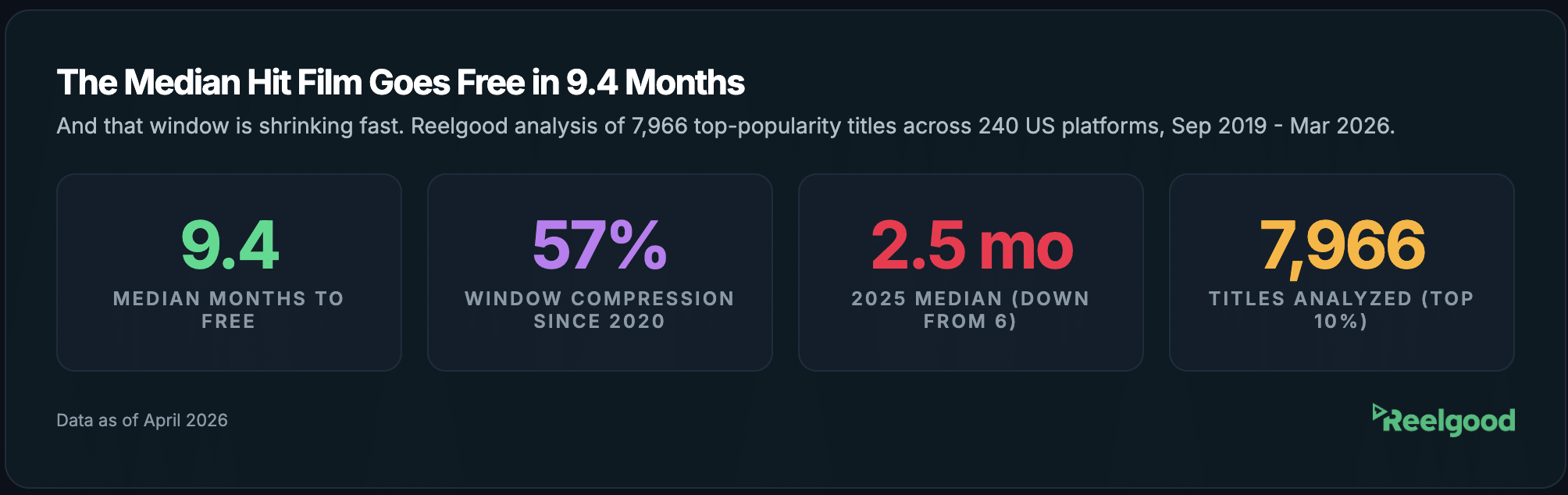

- The median time from a popular movie’s first paid availability to its first free/AVOD appearance is 9.4 months (including catalog titles already on paid platforms when tracking began). But that number is dropping fast: for 2025 releases, the median is just 2.5 months, down from 6 months in 2020.

- Studios play the windowing game very differently. Disney holds titles off free platforms for a median of 46 months. Sony/Columbia: 13 months. That 3.5x gap has direct implications for any acquisition team modeling rights windows by studio.

- Genre matters more than most models account for. Horror and thriller titles reach free platforms in under 5 months. Animation and children’s content takes nearly 3 years. If your windowing assumptions are genre-agnostic, they’re wrong.

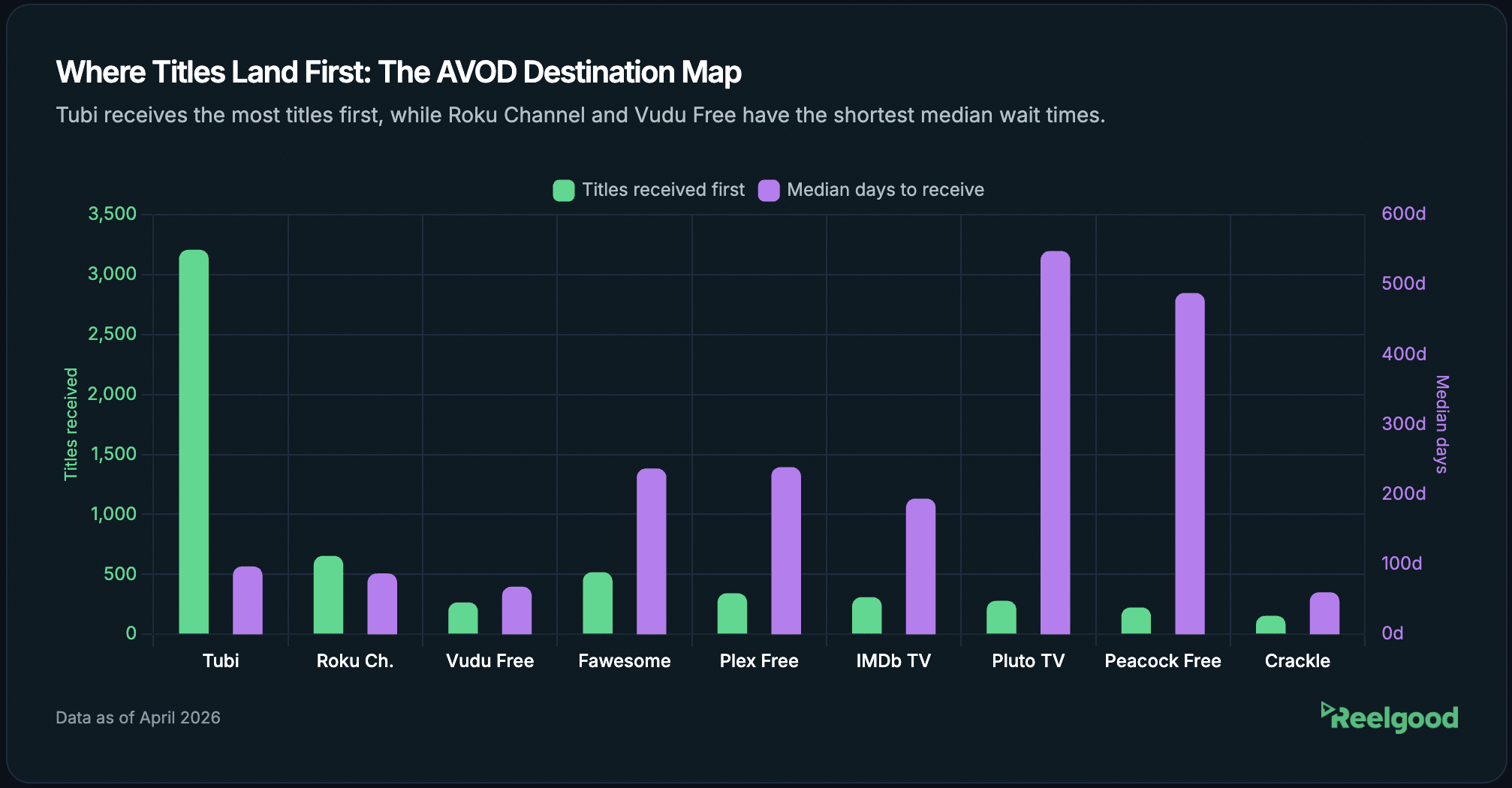

- Tubi is the dominant first-free destination, receiving more than 3,200 popular titles as their first free platform. Roku Channel and Vudu Free have the shortest median wait times (87 and 68 days, respectively).

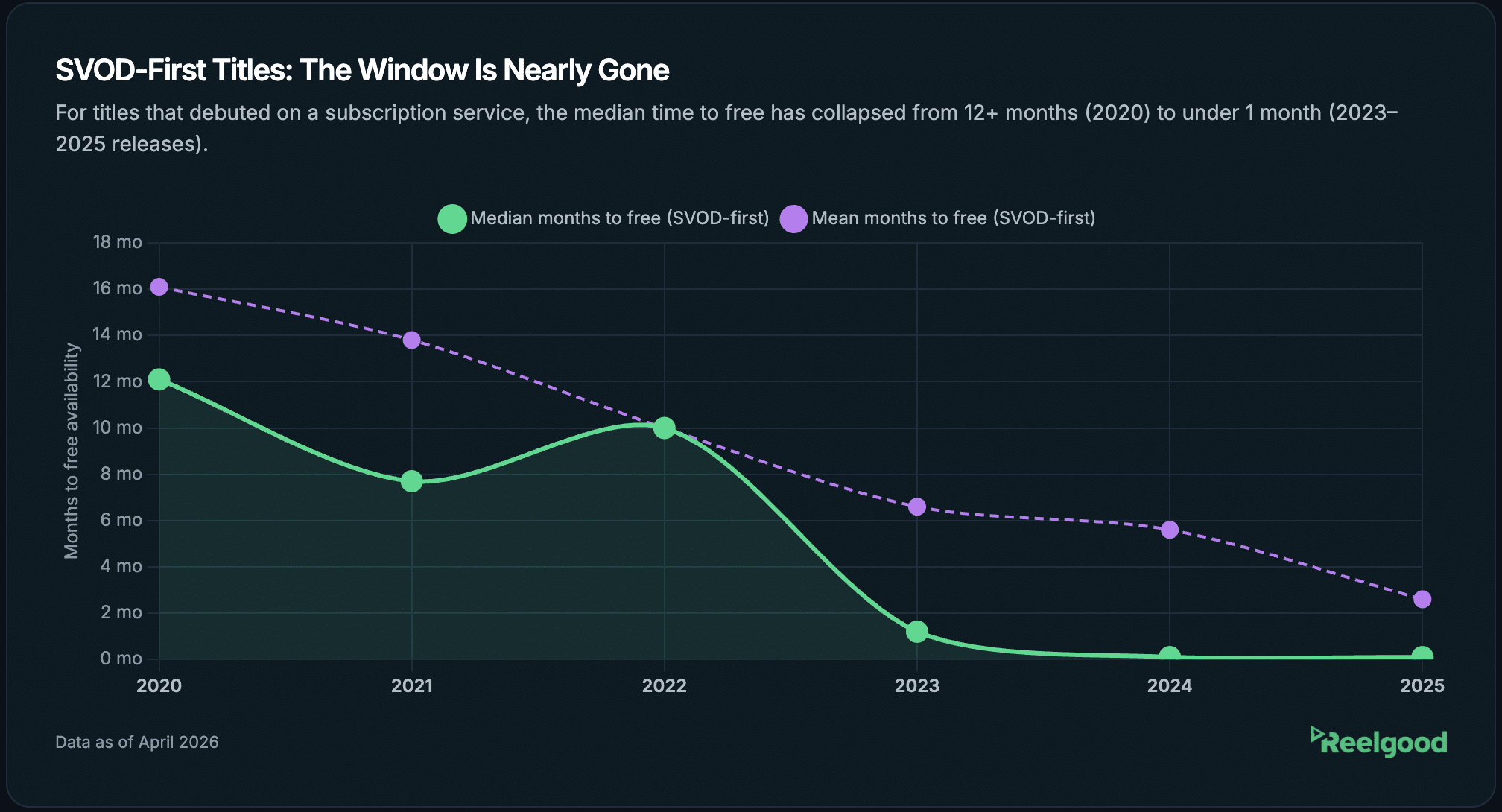

- For SVOD-first titles, the exclusivity window has nearly collapsed. Titles that debuted on a subscription service in 2023-2025 had a median time-to-free of under 1 month, down from 12 months for 2020 releases.

The Windowing Clock Runs Faster Than You Think

If you work in content acquisition or licensing, you have a mental model for how long a title stays behind a paywall before it appears on a free, ad-supported platform. That model is probably out of date.

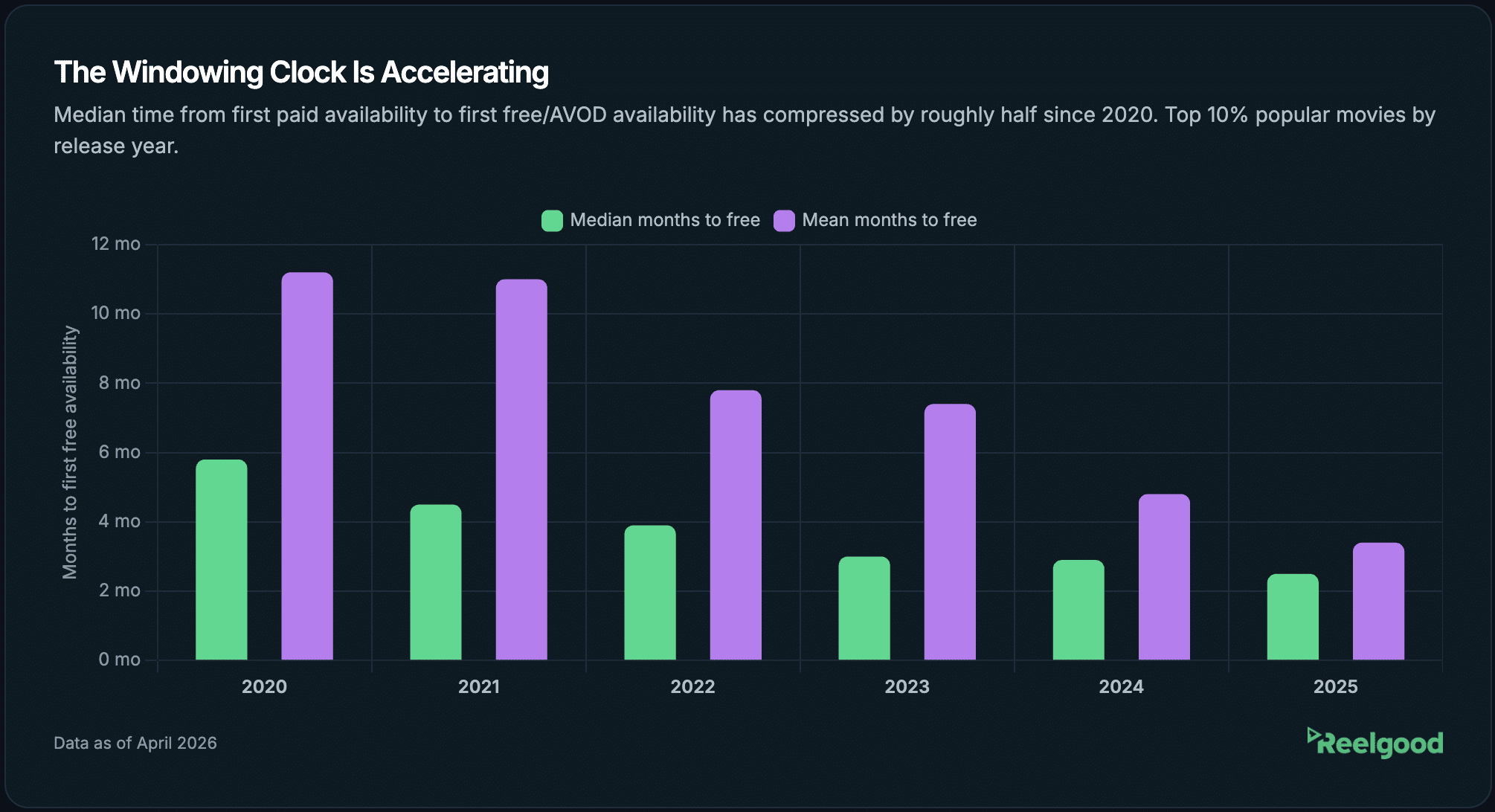

We analyzed 7,966 popular movies (the top 10% by Reelgood popularity score) that had a calculable path from paid to free availability across the US market. The overall median time-to-free is 9.4 months, but the more useful number is the trend line: that median has compressed by nearly 60% since 2020.

For movies released in 2020, the median gap between first paid appearance and first free/AVOD listing was 6 months. By 2022, it was 4 months. For 2025 releases, it’s 2.5 months. The mean tells a similar story, dropping from 11 months (2020) to 3.4 months (2025).

This isn’t a gradual drift.

It’s structural compression, driven by the rapid expansion of FAST (free ad-supported streaming television) services, increased competition for ad-supported eyeballs, and studio strategies that increasingly treat AVOD as a revenue layer rather than a last resort.

For licensing teams modeling rights windows, the implication is concrete:

The assumptions embedded in multi-year acquisition models may already be outdated.

A title that would have stayed exclusive to a subscription service for 12-18 months in 2020 may now reach free platforms in under 90 days.

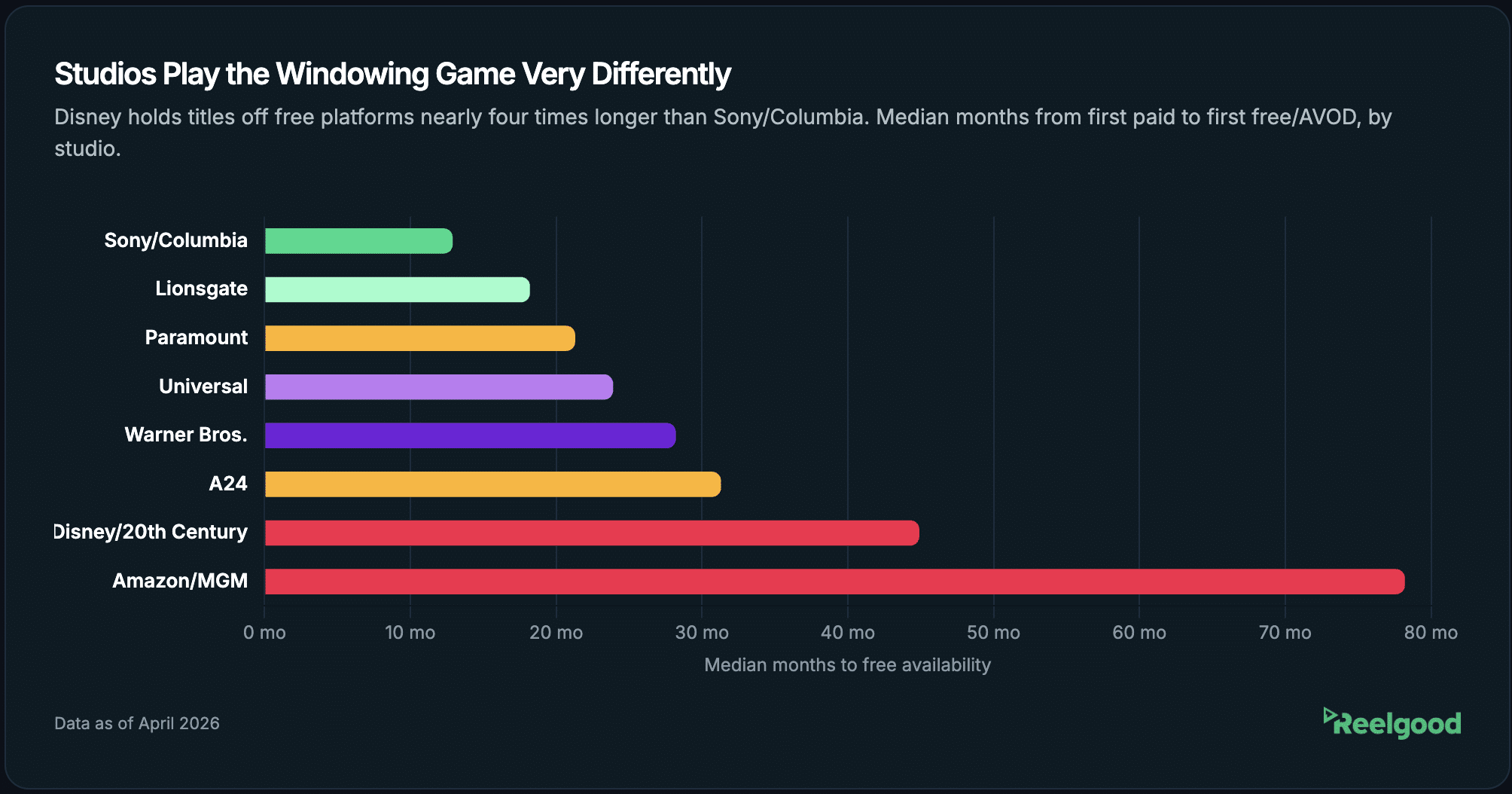

Disney Holds. Sony Releases. The Gap Is 3.5x.

Not all studios treat the windowing clock the same way.

When we segmented time-to-free by production company across the major studios, the spread was striking. Time-to-free here measures the gap from a title’s first paid availability (typically purchase/TVOD) to its first appearance on a free/ad-supported platform, covering the full paid lifecycle, not just the SVOD exclusivity period.

Sony/Columbia titles reach free platforms fastest among the majors, with a median of 13 months, though individual titles range widely: about 40% arrive on AVOD within 6 months, while roughly 20% take over 3 years. Lionsgate follows at 18 months, then Paramount (21.5 months), Universal (24 months), and Warner Bros. (28 months).

And then there’s Disney.

Titles from Disney and its subsidiaries (Pixar, Marvel, Lucasfilm, 20th Century Studios, Searchlight) have a median time-to-free of 44.9 months: nearly four years. That’s not just an outlier. It’s a fundamentally different distribution philosophy, one that treats the Disney brand itself as a windowing moat.

The practical consequence for content acquisition teams:

If you’re building a windowing model that treats “major studio” as a single category, you’re blending together strategies that differ by a factor of 3.5x.

A Sony action film and a Disney animation may both be “major studio releases,” but their path to AVOD availability has almost nothing in common.

This is exactly where historical streaming availability data becomes a strategic asset rather than a nice-to-have.

Studio-level windowing patterns only become visible when you have years of title-level availability records across hundreds of services, not spot checks or industry anecdotes.

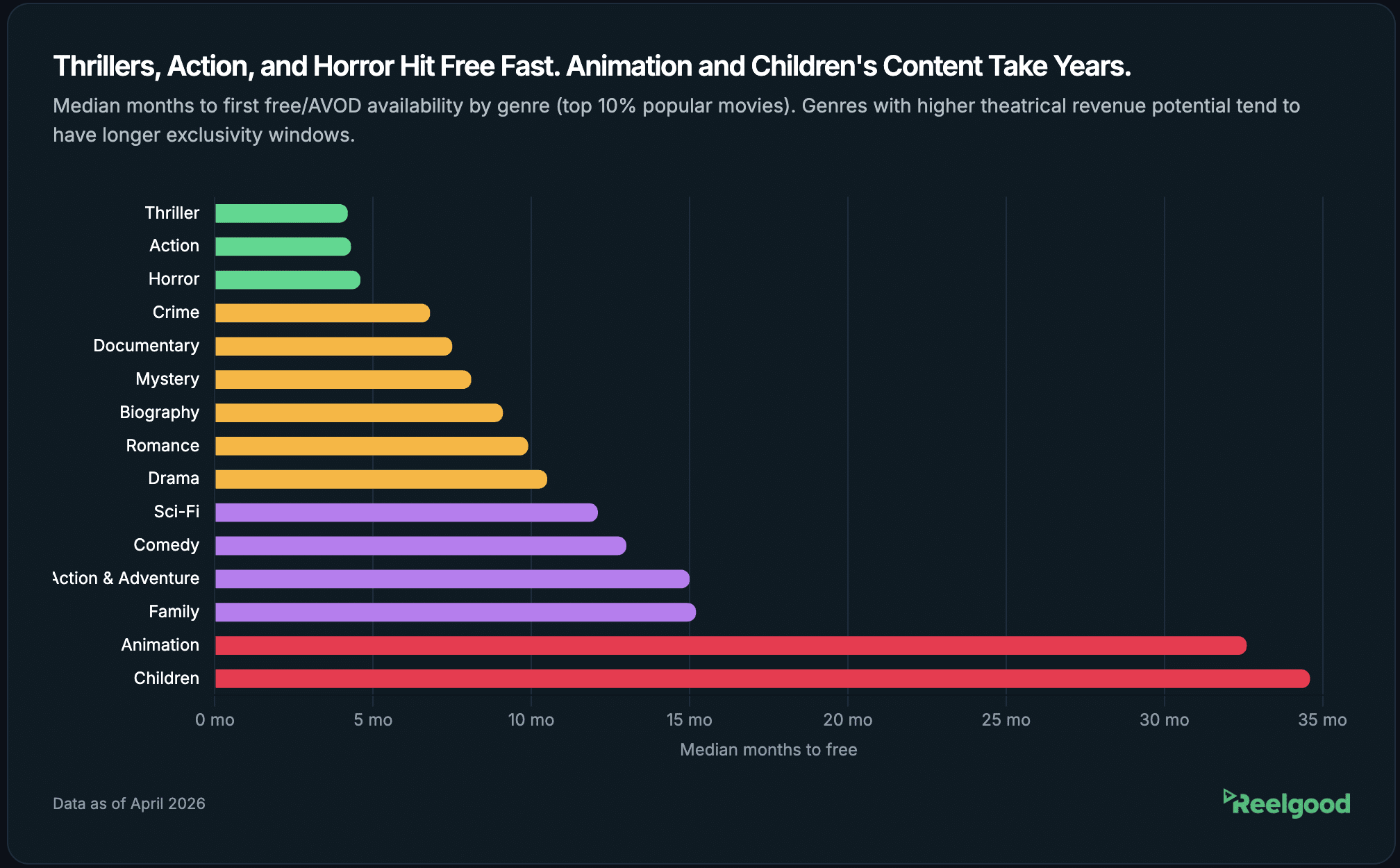

Genre Is a Hidden Variable in Windowing Models

Ask most people in content licensing how long a “hit movie” takes to reach AVOD, and they’ll give you a single number.

But the data shows that genre is one of the strongest predictors of windowing speed, and it’s routinely underweighted in acquisition models.

Horror and thriller titles reach free platforms in under 5 months (median 4.6 and 4.3 months, respectively). These genres have a short theatrical tail, lower rewatchability on subscription platforms, and a large, engaged audience on ad-supported services like Tubi and Pluto TV.

Action (4.4 months) and crime (6.8 months) follow a similar fast-to-free pattern. Documentaries and dramas sit in the middle range at 7.5 and 10.5 months.

At the other end of the spectrum: animation takes a median of 32.7 months to reach a free platform, and children’s content takes 34.6 months.

The economics here are straightforward.

Family content has longer lifecycle value on subscription platforms (parents renew for it), and studios invest more heavily in protecting those franchises. A title like Sing 2 (which took over 23 months from its first paid window to its first free listing) isn’t an anomaly. It’s the standard for the genre.

For rights management teams tracking licensing compliance,

This means the “expected” window for a title depends heavily on what kind of title it is.

A genre-blind monitoring approach will generate noise: flagging horror titles as unexpectedly early on AVOD, or missing that an animated film has appeared on a free service ahead of its expected window.

Tubi Wins the Volume Race. Roku Channel Wins on Speed.

When popular titles finally land on a free platform, where do they go first?

Tubi is the clear volume leader, receiving 3,188 popular titles as their first free destination: more than the next four AVOD platforms combined. Tubi’s median wait time is 97 days from a title’s first paid appearance, which places it in the middle of the pack on speed.

Roku Channel (654 titles, 87-day median) and Vudu Free (266 titles, 68-day median) get titles slightly faster but at lower volume. Crackle has the shortest median wait at just 60 days, though with a much smaller sample of 154 titles.

At the other extreme, Pluto TV (548-day median) and Peacock Free (488-day median) tend to receive titles much later in the distribution cycle. These platforms may be picking up titles in secondary or tertiary free windows rather than as initial AVOD destinations.

For product and content teams at AVOD services, this data matters for competitive positioning.

If you’re a Pluto TV content strategist, knowing that Tubi consistently gets the same titles 400+ days earlier is an

Actionable competitive intelligence gap.

And for content search and discovery teams building “where to watch” features, the rapid migration of titles across free platforms makes real-time availability data a hard requirement, not a nice-to-have.

[please note this is based on historical data; some of these services no longer exist or exist in different forms.]

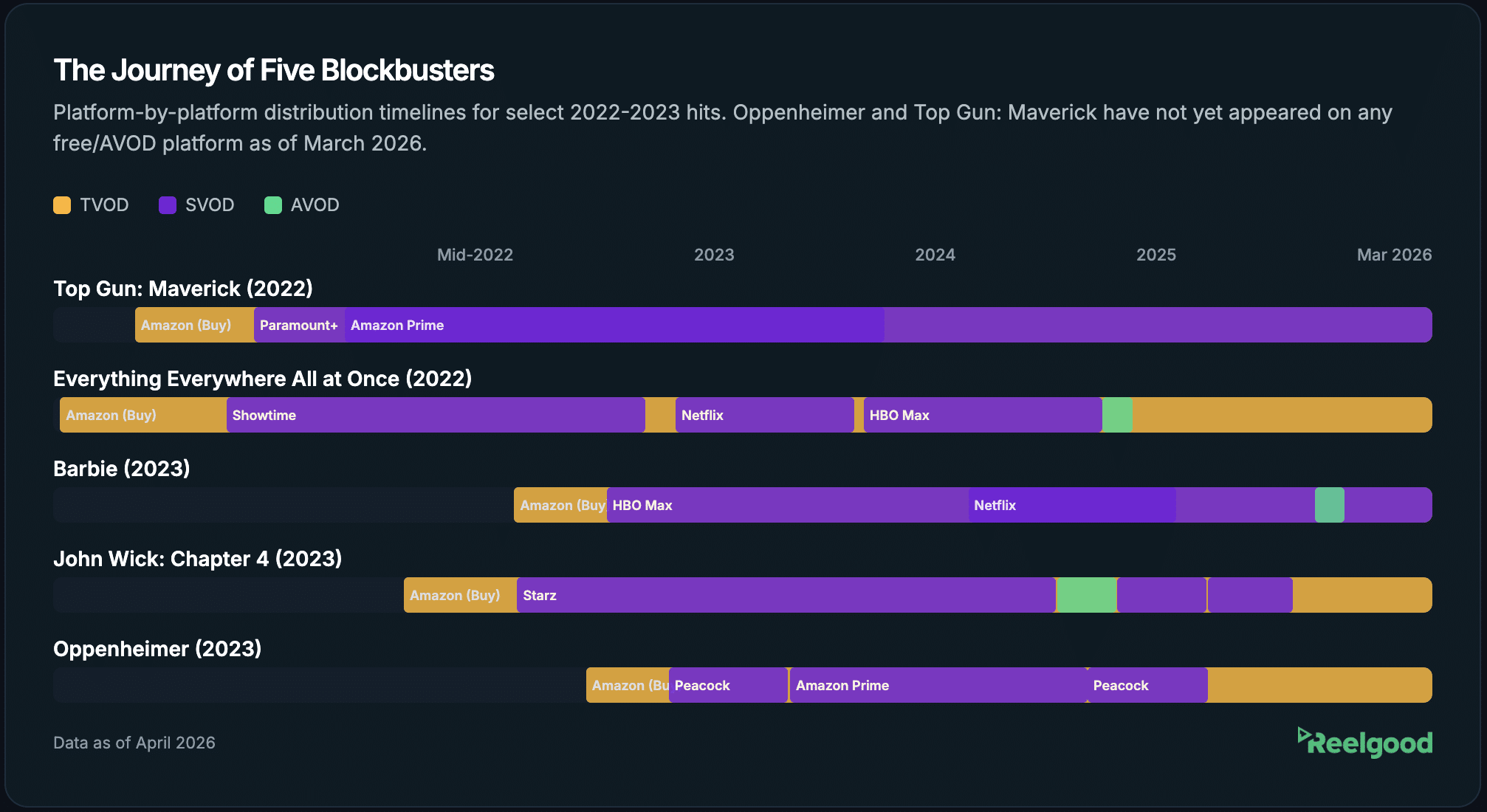

The Blockbuster Journey: Five Titles, Five Different Arcs

The aggregate data tells the structural story.

But individual title journeys show how varied and complex the distribution arc actually is.

Here are five recent blockbusters, traced through Reelgood’s historical availability data:

Barbie (2023): Available for purchase on Amazon in September 2023, about two months after its theatrical debut. HBO Max picked it up for SVOD in December 2023. Netflix ran it for a limited window from December 2024 to July 2025. But the first free/AVOD appearance didn’t come until December 2025 on Tubi: over 26 months after the first digital availability. For a title this commercially massive, that’s a textbook example of Warner Bros. protecting SVOD exclusivity for as long as possible before allowing ad-supported distribution.

John Wick: Chapter 4 (2023): Purchase availability in May 2023. Starz (SVOD) from September 2023 through March 2025. Then a brief two-month appearance on Roku Channel’s free tier (March-May 2025) before rotating through Peacock and Hulu. By early 2026, the title had cycled through six different SVOD services with multiple intermittent free windows on Roku Channel and Philo Free. John Wick’s path is a textbook example of a title bouncing between subscription services with brief free windows in between: complex, hard to predict, and hard to model.

Everything Everywhere All at Once (2022): Purchase from June 2022. Showtime (SVOD) from November 2022. Then Netflix for six months in early 2024, HBO Max for eight months, and finally a one-month free window on Tubi in May 2025. Nearly three years from first availability to first free listing: the slow burn of a prestige title.

Oppenheimer (2023): Purchase in November 2023, then Peacock (SVOD) from February through June 2024, followed by Amazon Prime from June 2024 through April 2025, and Peacock again from April through August 2025. As of March 2026, Oppenheimer has not appeared on any free/AVOD platform. Like Top Gun: Maverick, it remains locked in the subscription/purchase ecosystem. For a Universal title, this is notable: Universal’s overall median time-to-free is 24 months, but Oppenheimer at 28+ months and counting is being held tighter than the studio average.

Top Gun: Maverick (2022): Purchase from May 2022, Paramount+ (SVOD) from December 2022. As of March 2026, Maverick has not appeared on any free/AVOD platform. It remains locked within the Paramount ecosystem: a premium holdback that reflects Paramount’s strategy of using tentpole titles to protect subscriber value.

These five titles represent four different windowing philosophies:

- Warner’s long SVOD-first hold (Barbie),

- Lionsgate’s rotational churn with free gaps (John Wick),

- the prestige slow burn (Everything Everywhere),

- and the premium holdback that may never go free (Oppenheimer, Top Gun).

No single model captures them all, which is precisely why

Historical, title-level availability data is more useful than industry averages.

The SVOD Exclusivity Window Is Nearly Gone

Perhaps the most dramatic finding in the data:

For titles that debuted on a subscription service (SVOD-first, rather than starting on purchase/TVOD), the exclusivity window before free availability has nearly vanished.

In 2020, SVOD-first titles had a median time-to-free of 12 months. By 2021, it dropped to 8 months. By 2023, the median fell to just over 1 month. And for 2024-2025 SVOD-first releases, the median is essentially zero: titles are appearing on free platforms within days of their subscription debut. The mean has also plummeted, from 16 months (2020) to 2.6 months (2025).

This likely reflects the growth of platforms like Roku Channel and Tubi that have output agreements allowing near-simultaneous free availability, as well as the proliferation of subscription services (like Cineverse) that have both paid and free tiers, where a title may appear on both simultaneously.

The SVOD-first exclusivity window is collapsing through two parallel shifts. First, services that operate both paid and free tiers (Roku, Peacock, Cineverse, Amazon/Freevee) increasingly launch titles across both tiers at or near the same time. Second, even for titles where the free platform is operated by a different company than the SVOD service, the gap has compressed from 16 months for 2020 releases to under 2 months for 2025.

For rights management teams, this trend has a direct operational consequence.

If you’re monitoring where your titles appear and whether they’re within their licensed windows, the margin for error has compressed dramatically. A title that’s “supposed to be” SVOD-exclusive may appear on a free tier within days, and

Distinguishing authorized from unauthorized distribution requires real-time monitoring, not quarterly audits.

As we noted in our analysis of the measurement gap in streaming, the tools most teams use for competitive intelligence and rights compliance were built for a slower-moving market. The data suggests that market is gone.

What This Means for Your Team

The distribution arc of a movie in 2026 is faster, more complex, and more studio- and genre-dependent than the industry’s standard windowing assumptions account for. The data points to three specific implications:

For content acquisition and licensing teams:

Your windowing models need studio-level and genre-level granularity. An “average” window of 9-12 months masks a reality where Sony horror titles hit AVOD in 4 months and Disney animations take 3+ years. Reelgood’s historical availability data can provide the title-level, platform-level records your models need.

For rights management teams:

The SVOD-to-free window is compressing to near-zero for many titles. If your compliance monitoring runs on anything slower than real-time, you’re likely missing unauthorized availability events. Reelgood tracks availability across 300+ services globally, updating every few minutes.

For AVOD product and content teams:

Tubi’s dominance as the first-free destination is quantifiable, and so are the speed advantages of Roku Channel and Vudu Free. If you’re competing for AVOD catalog share, knowing where titles land first (and how quickly) is competitive intelligence you need.

What Should You Do?

If your team is making licensing, acquisition, or compliance decisions without title-level historical availability data, you’re working from assumptions that the market has already moved past. Reach out to the Reelgood data team to explore how our historical and real-time availability data can sharpen your windowing analysis.

Data: Reelgood Movie & TV Metadata & Streaming Availability Database, March 2026. Analysis covers the US market. “Popular movies” defined as the top 10% by Reelgood popularity score (~18,800 unique titles; 7,966 with calculable paid-to-free paths). Availability windows span September 2019 through March 2026 across 240 streaming platforms. Titles already on paid platforms when tracking began in September 2019 have a left-censored first paid date, which contributes to a higher overall median (9.4 months) than the year-by-year trend (as seen in “The Windowing Clock is Accelerating” chart) for recent releases. The analysis only includes titles that have appeared on both paid and free platforms. Titles that remain exclusively on paid services are not represented, which means actual studio-level time-to-free for all titles may be longer than reported.

Business model classified by source_id suffix (TVOD/SVOD/AVOD). Time-to-free calculated as the gap between first paid (SVOD or TVOD) appearance and first free/ad-supported (AVOD) appearance for each title.